The automobile sector is a critical pillar of Pakistan’s industrial economy, serving as a barometer for middle-class consumption and domestic supply chain maturity. Historically characterized by a high degree of import-reliance, the industry has undergone a strategic albeit volatile pivot toward domestic assembly. This transition is underpinned by fiscal policies designed to incentivize localization and mitigate the impact of persistent foreign exchange constraints. Central to this ecosystem are the Pakistan Automotive Manufacturers Association (PAMA) and the Pakistan Association of Automotive Parts & Accessories Manufacturers (PAAPAM), which provide the regulatory and quality-assurance frameworks necessary for large-scale industrialization.

The sector is structurally divided into Automobile Assemblers (Original Equipment Manufacturers) and Automobile Parts & Accessories manufacturers. These sub-sectors exhibit a symbiotic but increasingly divergent relationship: while the assemblers drive top-line growth through new model introductions and localized assembly, the parts manufacturers provide the critical infrastructure for value addition. This analysis provides a meticulous year-on-year (YoY) financial appraisal from 2021 to 2025, utilizing bottom-up data to navigate through reporting discrepancies and provide institutional-grade insights into the sector’s strategic trajectory.

Sector Composition and Market Hierarchy

For institutional investors, the Pakistan Stock Exchange (PSX) classification system is the primary tool for benchmarking liquidity and corporate maturity. Inclusion in the FSE 100 Index typically denotes superior asset utilization and market trust. The following hierarchy identifies the tiering within the sector, including prominent unlisted entities that define the market's depth.

Market Hierarchy & PSX Index Rating

| S.No | Company Name | Sector Classification | FSE 100 Index Rating | Corporate Status |

| 1 | Millat Tractors Limited | Automobile Assembler | 21 | Active |

| 2 | Sazgar Engineering Works Ltd | Automobile Assembler | 22 | Active |

| 3 | Indus Motor Company Limited | Automobile Assembler | 35 | Active |

| 4 | Thal Limited | Parts & Accessories | 50 | Active |

| 5 | Atlas Honda Limited | Automobile Assembler | 53 | Active |

| 6 | Ghandhara Industries Limited | Automobile Assembler | 71 | Active |

| 7 | Ghandhara Automobiles Ltd | Automobile Assembler | 78 | Active |

| 8 | Honda Atlas Cars (Pakistan) Ltd | Automobile Assembler | 90 | Active |

| 9 | Atlas Battery Limited | Parts & Accessories | Not Listed | Active |

| 10 | Exide Pakistan Limited | Parts & Accessories | Not Listed | Active |

| 11 | Panther Tyres Limited | Parts & Accessories | Not Listed | Active |

| 12 | Dewan Farooque Motors Limited | Automobile Assembler | Not Listed | Non-Compliant |

Top-tier entities like Millat Tractors and Sazgar Engineering command the highest index weights, reflecting high liquidity and institutional confidence. The inclusion of parts manufacturers like Thal Limited (Rating 50) suggests that certain downstream players have achieved the scale necessary to compete for institutional capital. However, the presence of non-compliant entities like Dewan Farooque Motors underscores a significant delisting risk and a total loss of liquidity for minority shareholders.

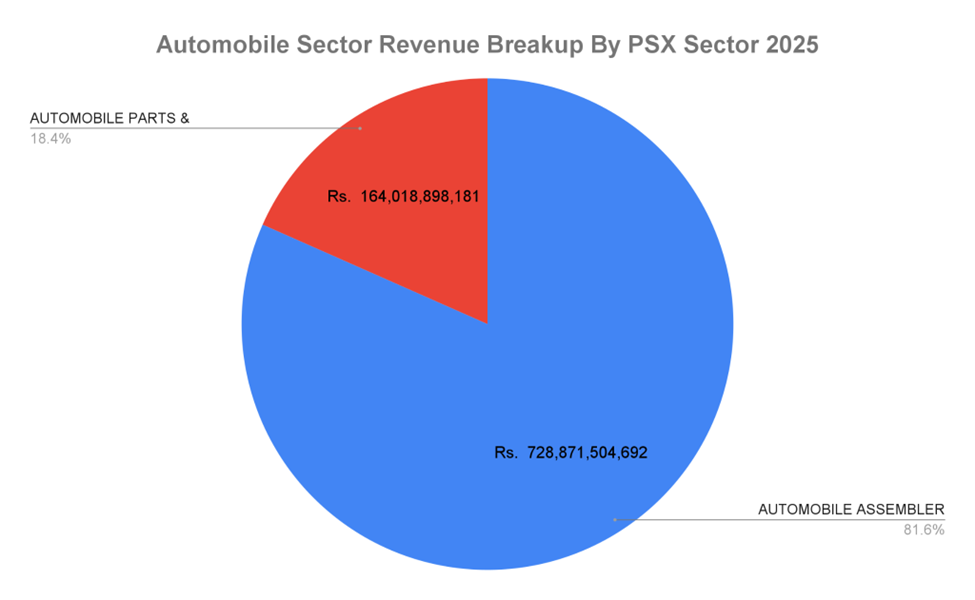

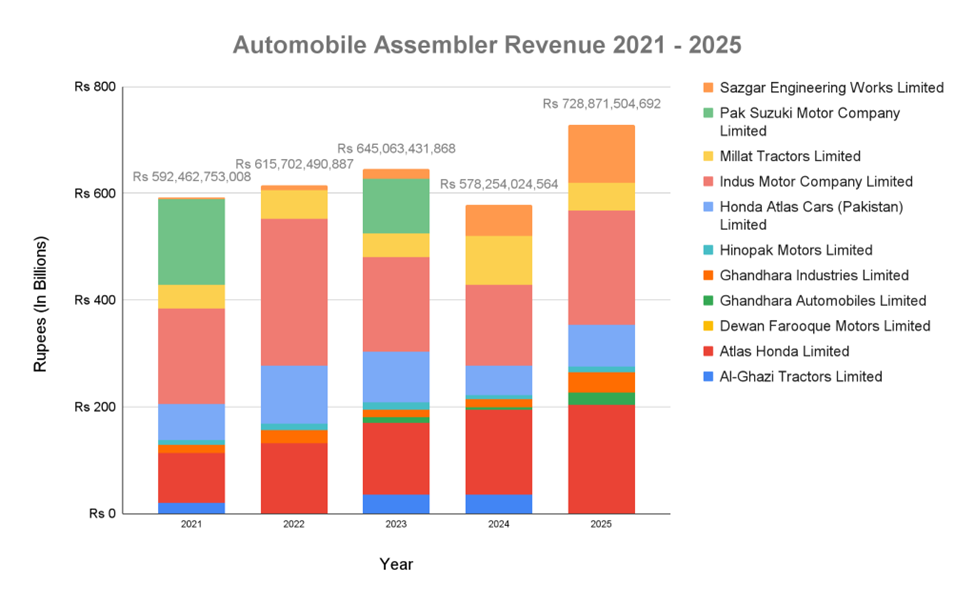

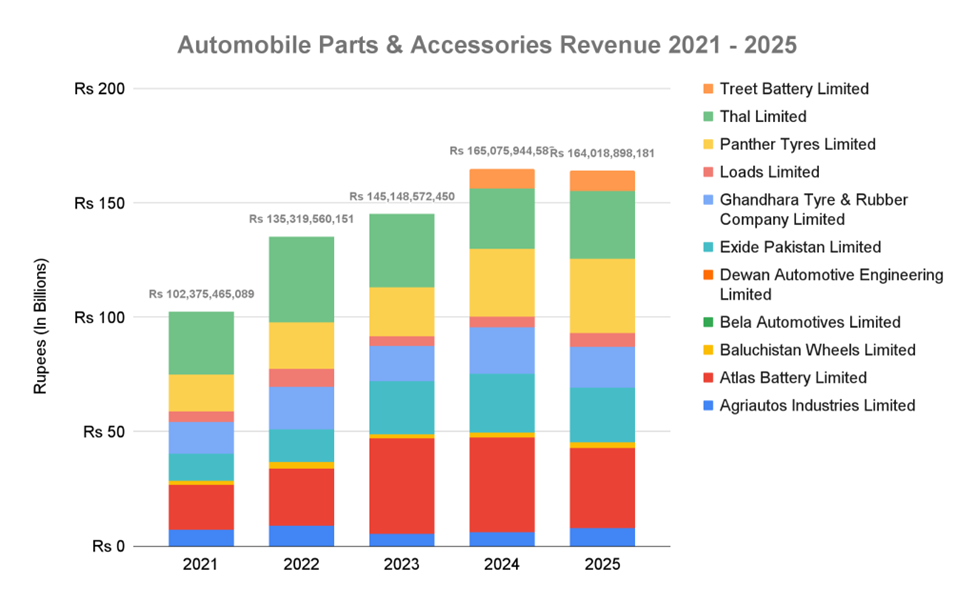

Revenue Performance

The revenue trajectory of the last five years has been defined by extreme macroeconomic headwinds, including severe PKR devaluation and import restrictions.

- Assembler Resilience and Low-Base Recovery: After a 10.36% dip in 2024 (Rs. 578.2B), the Assembler sub-sector staged a massive 26.05% recovery in 2025, reaching Rs. 728.8B. This growth must be contextualized within the 2023–2024 "Assembler Dip," where high interest rates and government tariffs on finished imports forced a contraction. The 2025 surge represents a low-base effect as production normalized.

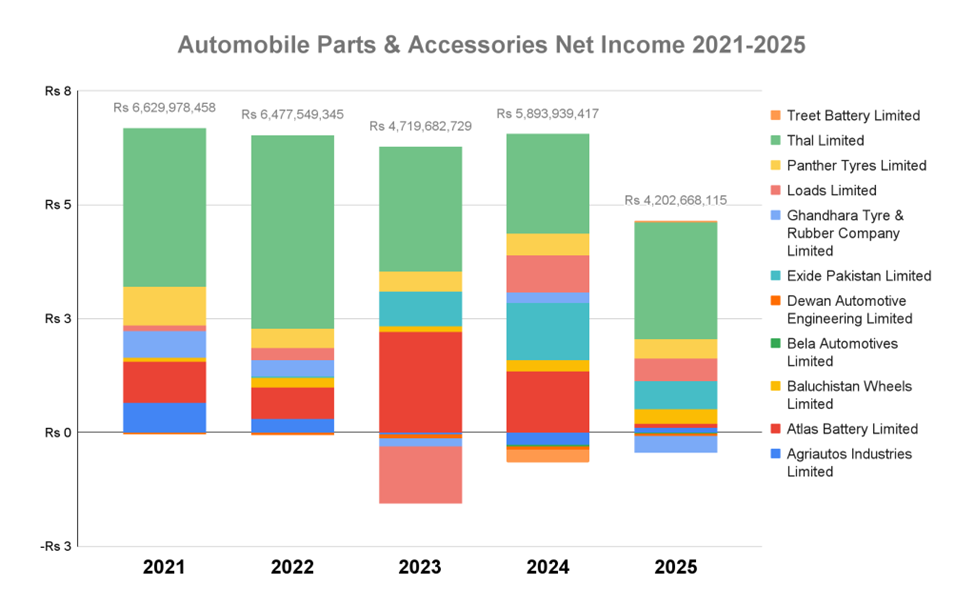

- Parts & Accessories Stagnation: In contrast, the Parts sector saw a 32.18% surge in 2022 but has since entered a phase of relative stagnation, ending 2025 with a marginal -0.64% decline (Rs. 164.0B).

Strategic Interpretation: The divergence in 2025 indicates a "top-heavy" recovery. Assemblers are successfully capturing the "New Car" demand driven by model refreshes and localized assembly incentives. However, the stagnation in the Parts sub-sector suggests a significant margin squeeze; parts manufacturers are increasingly unable to pass on inflationary costs and raw material price hikes to the Assemblers, who maintain superior bargaining power in the value chain.

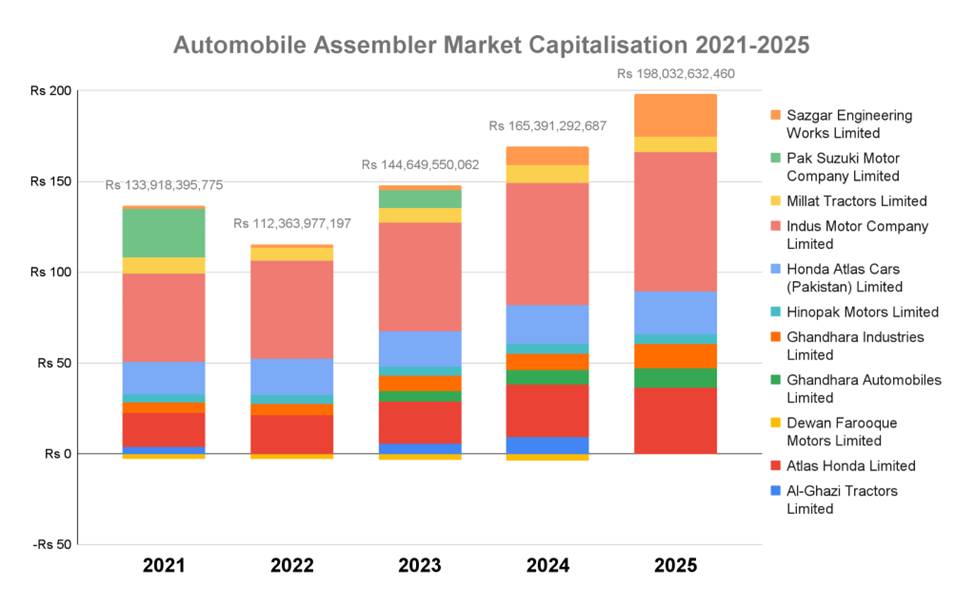

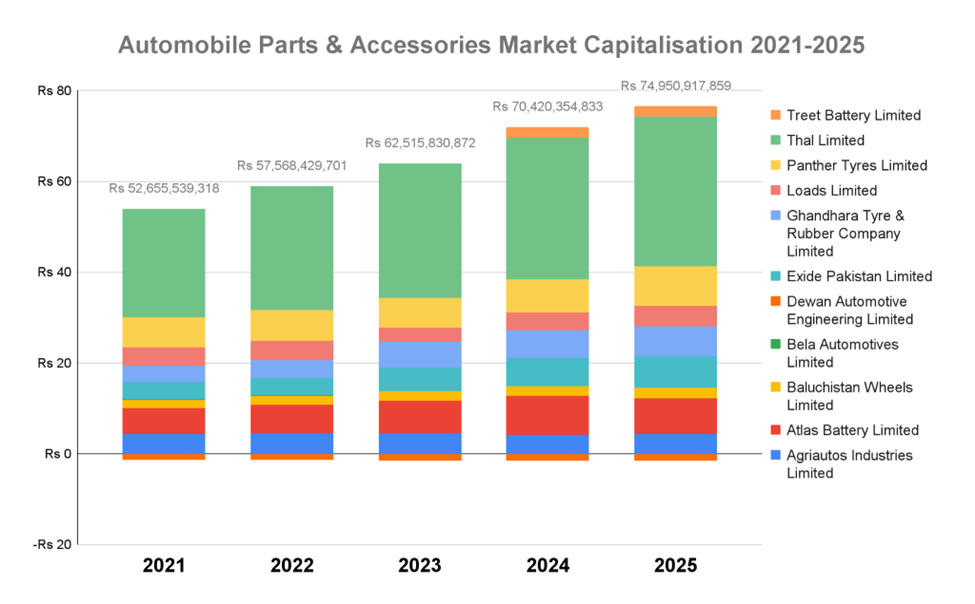

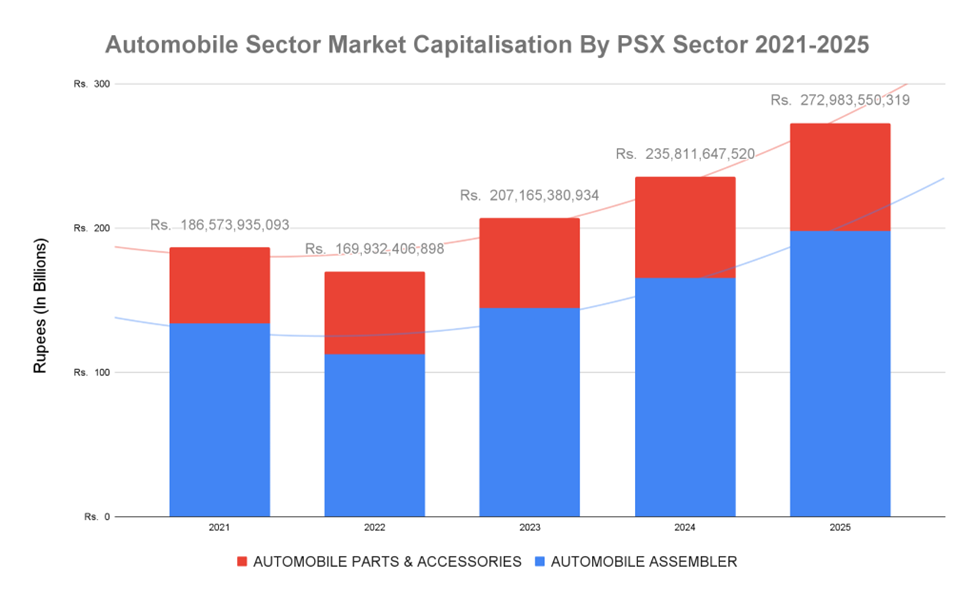

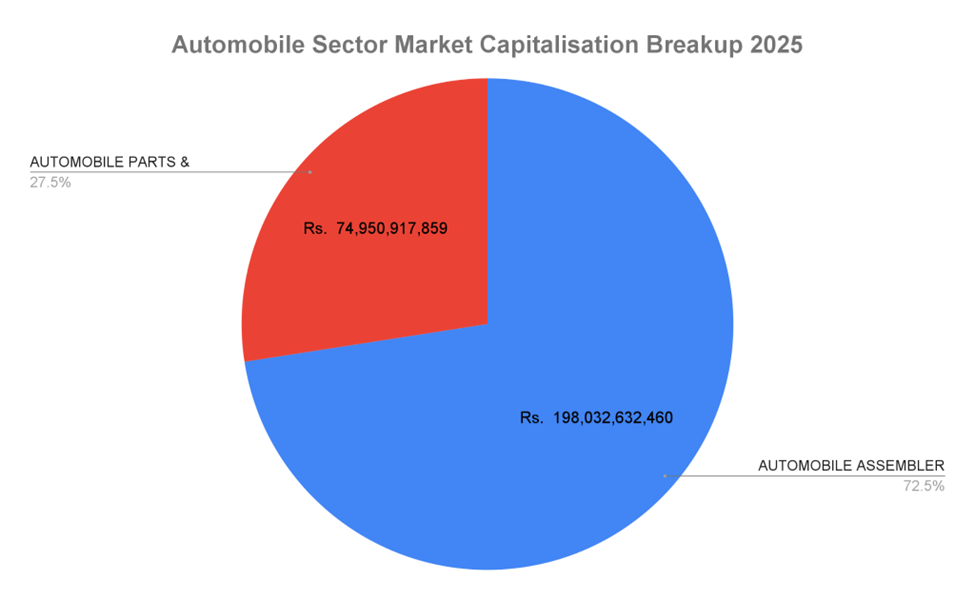

Market Capitalization

Market capitalization serves as the ultimate metric of investor expectations regarding future growth and delisting risk.

- Automobile Assemblers: Investor sentiment has turned aggressively bullish, with a 28.73% jump in 2023 followed by a 19.74% rise in 2025, bringing the segment to Rs. 198.03B.

- Parts & Accessories: Growth has been steadier but far less dynamic, posting a 6.43% rise in 2025 to reach Rs. 74.95B.

The "Suzuki Factor" and Market Concentration: A critical shift in the 2024–2025 data is the disappearance of Pak Suzuki Motor Company Limited from active market metrics. This indicates a significant corporate delisting or buyback event, which has redistributed market concentration toward Indus Motor Company (Rs. 76.95B) and Atlas Honda (Rs. 36.36B). Investors are increasingly concentrating capital in "blue-chip" assemblers with high asset utilization, viewing them as safer havens against fiscal volatility.

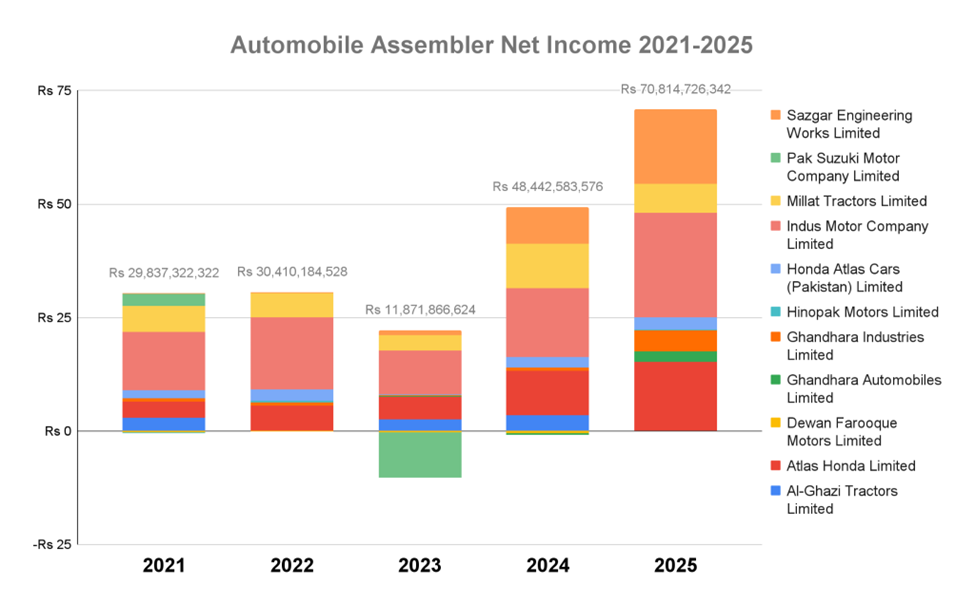

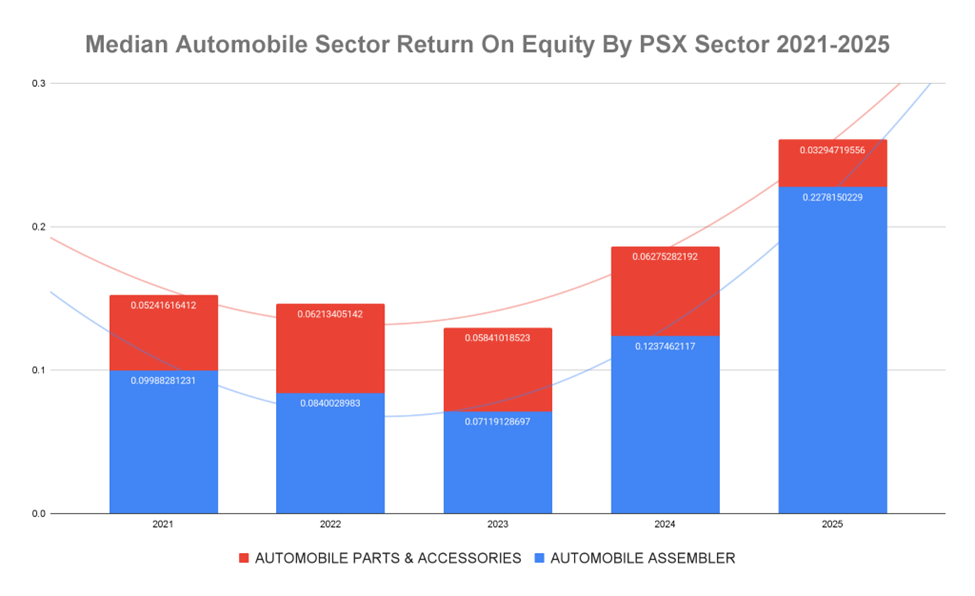

Profitability and Efficiency: Net Income & Return on Equity (ROE)

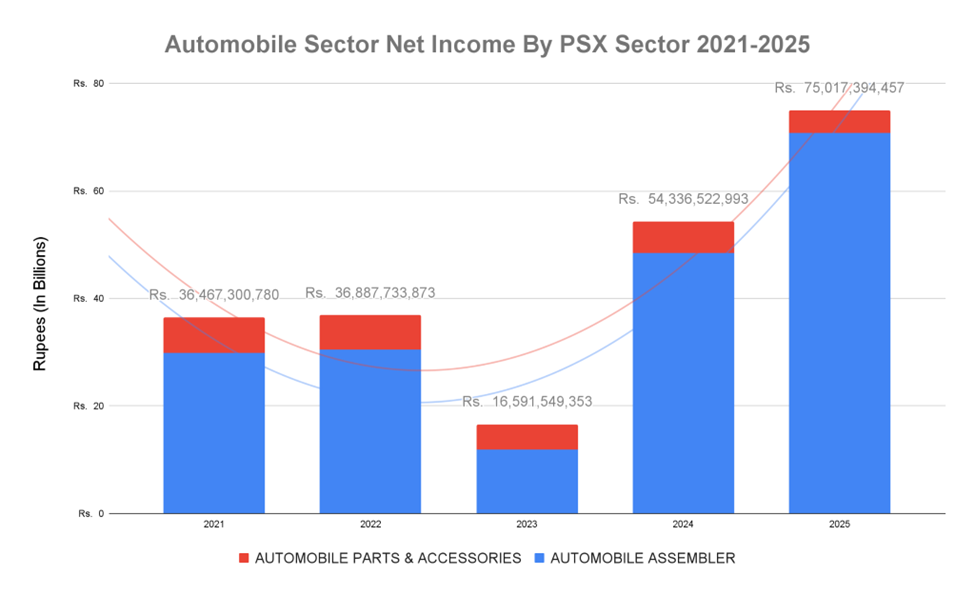

Bottom-line performance reveals the true impact of operating leverage. The 308.05% surge in Assembler net income in 2024 was a technical rebound from the disastrous 2023 crash (-60.96%), where PKR devaluation decimated margins.

Sector Net Income YoY Change (%) & Combined Totals

| Year | Assembler YoY % | Parts YoY % | Combined Net Income (Rs.) |

| 2025 | 46.18% | -28.70% | Rs. 75.01B |

| 2024 | 308.05% | 24.88% | Rs. 54.33B |

| 2023 | -60.96% | -27.14% | Rs. 16.59B |

| 2022 | 1.92% | -2.30% | Rs. 36.88B |

While Assemblers maintained profitability through 2025, Parts manufacturers suffered a sharp -28.70% contraction. This reinforces the "margin squeeze" narrative, as downstream players absorb the costs of supply chain shocks.

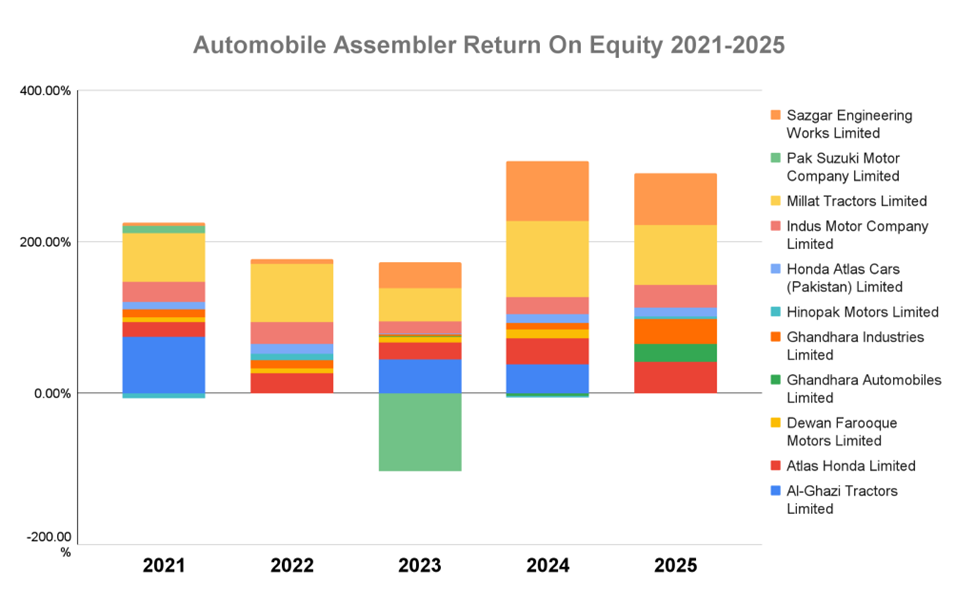

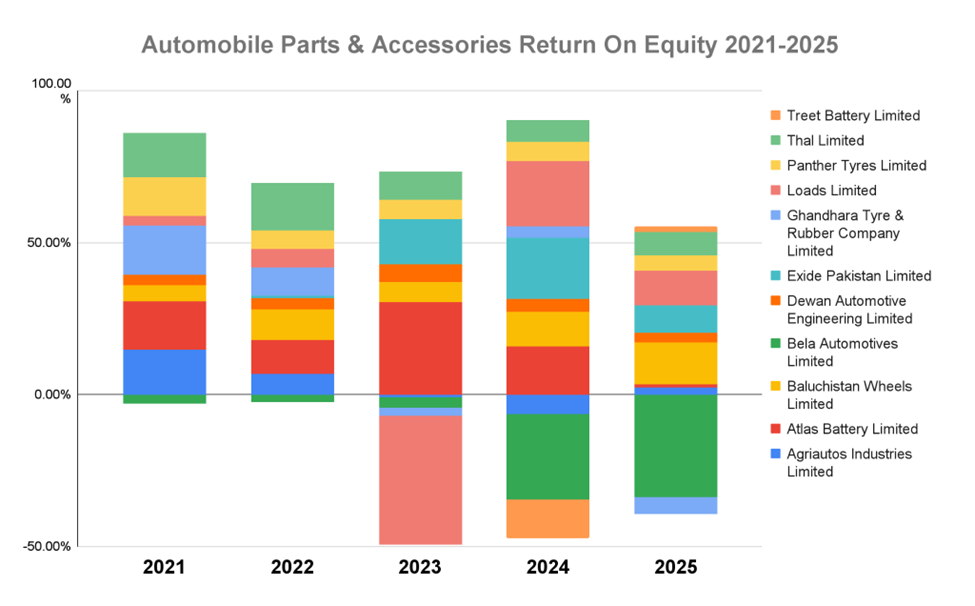

Elite Capital Efficiency (2024 ROE): Institutional investors prioritize Return on Equity (ROE) as the definitive measure of management's ability to generate profit from shareholder funds.

- Millat Tractors (MTL): Recorded a dominant ROE of 1.02 in 2024, the highest in the industry.

- Sazgar Engineering (SAZEW): Posted an impressive 0.79, signaling elite-tier asset utilization during a period of expansion.

- Vulnerability: Conversely, Bela Automotives continues to signal distress with a negative ROE of -0.34 in 2025, reflecting a persistent lack of operational viability.

Corporate Deep Dives: High Performers vs. Vulnerable Entities

Individual corporate narratives explain the delta between the sub-sectors.

- Sazgar Engineering Works: The sector's "alpha" performer. Sazgar’s revenue skyrocketed from Rs. 4.0B in 2021 to Rs. 108.6B in 2025—a meteoric 2,615% growth. This is not merely a market recovery but a disruptive shift likely driven by successful localization of new SUV models and high operating leverage.

- Indus Motor Company: Remains the revenue anchor (Rs. 215.1B in 2025). Its ability to maintain a 0.30 ROE in 2025 suggests a robust defensive posture against macroeconomic shocks.

- Vulnerable Players: The "Non-Compliant/Winding Up" status of Dewan Farooque Motors and Bela Automotives serves as a stark warning. For institutional investors, these entities represent a total loss of liquidity and high delisting risk.

Conclusion

The Pakistan automobile sector has entered a "Recovery and Consolidation" phase. The Assembler sub-sector has emerged from the 2023 currency crisis with improved pricing power and significant net income growth. However, the structural weakness of the Parts & Accessories segment poses a systemic risk to the long-term sustainability of this recovery.

Future Considerations for Institutional Investors:

- The Parts Sector Margin Squeeze: Without the ability to pass on costs to Assemblers, Parts manufacturers face a "Middle Income Trap" that may lead to further consolidation or insolvency among smaller players.

- ROE Sustainability: The exceptionally high ROE levels of Millat (1.02) and Sazgar (0.79) are likely to mean-revert as competition intensifies and localization incentives are phased out.

- Fiscal and Exchange Risk: The sector remains highly sensitive to PKR stability. Any further devaluation will immediately trigger margin compression across both sub-sectors.

The resilience of the major assemblers is evident, but the path to 2026 depends on whether the industry can foster a more equitable distribution of profitability across the entire value chain.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.