In the Pakistan Stock Exchange, all listed companies operating in the steel industry are classified in the “Engineering” sector. There are 20 publicly listed companies operating in the segment. The top players in the sector with a market capitalisation of more Rs. 10 Billion each are Mughal Iron & Steel Industries Limited, International Steels Limited, Agha Steel Ind.Ltd, Aisha Steel Mills Limited, International Industries Limited and Amreli Steels Limited.

Overview

The steel sector constitutes the industrial backbone of Pakistan, serving as a high-fidelity barometer for infrastructure health and macroeconomic stability. Between 2021 and 2025, this sector underwent a catastrophic transition from a "surplus era" of peak profitability to a state of systemic insolvency risk. While 2021–2022 was characterized by robust margins and scale, the subsequent years reveal a sector-wide collapse in operational viability. By 2025, the industry is projected to enter a definitive "deficit era," where the aggregate Return on Equity (ROE) remains incalculable due to the total erosion of the sector's equity base. This is no longer a standard cyclical downturn; it is a fundamental breakdown of the sector's financial architecture.

Aggregate Sector Performance Metrics

| Year | Market Capitalization | Revenue | Net Income |

| 2021 | Rs. 103.92 billion | Rs. 280.91 billion | Rs. 23.53 billion |

| 2022 | Rs. 118.36 billion | Rs. 373.42 billion | Rs. 17.91 billion |

| 2023 | Rs. 126.94 billion | Rs. 294.09 billion | Rs. 5.49 billion |

| 2024 | Rs. 146.73 billion | Rs. 311.00 billion | (Rs. 3.95 billion) |

| 2025 | Rs. 149.11 billion | Rs. 256.41 billion | (Rs. 8.08 billion) |

The precipitous drop in aggregate profitability against a shrinking revenue base suggests a volatile operational environment that has pushed several major players toward a solvency crisis.

Revenue Dynamics

Revenue stability is the primary indicator of industrial absorption and capacity utilization. The extreme fluctuations observed between 2022 and 2025 signal severe economic instability, driven by contracting domestic demand and escalating input costs.

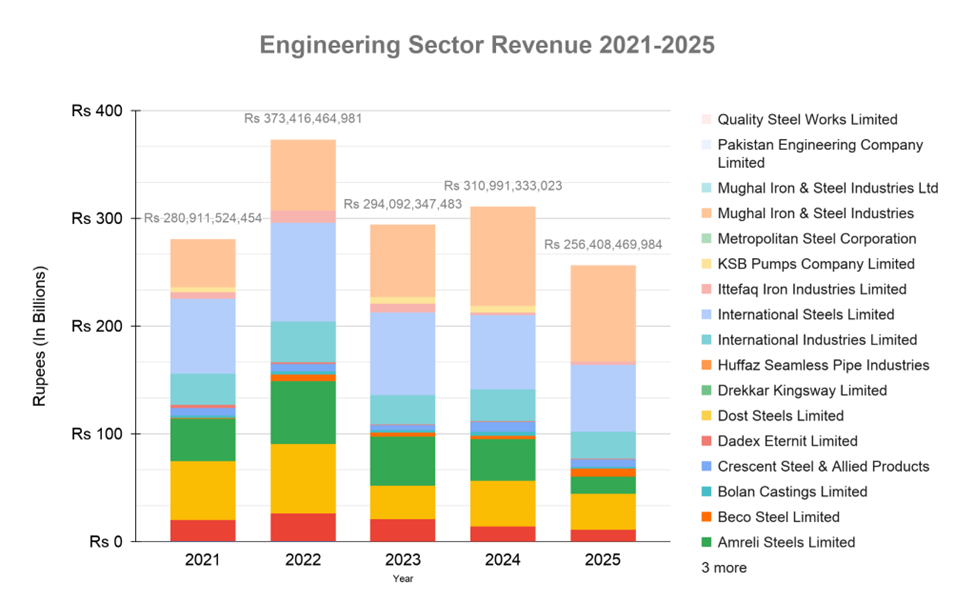

(See chart Revenue 1)

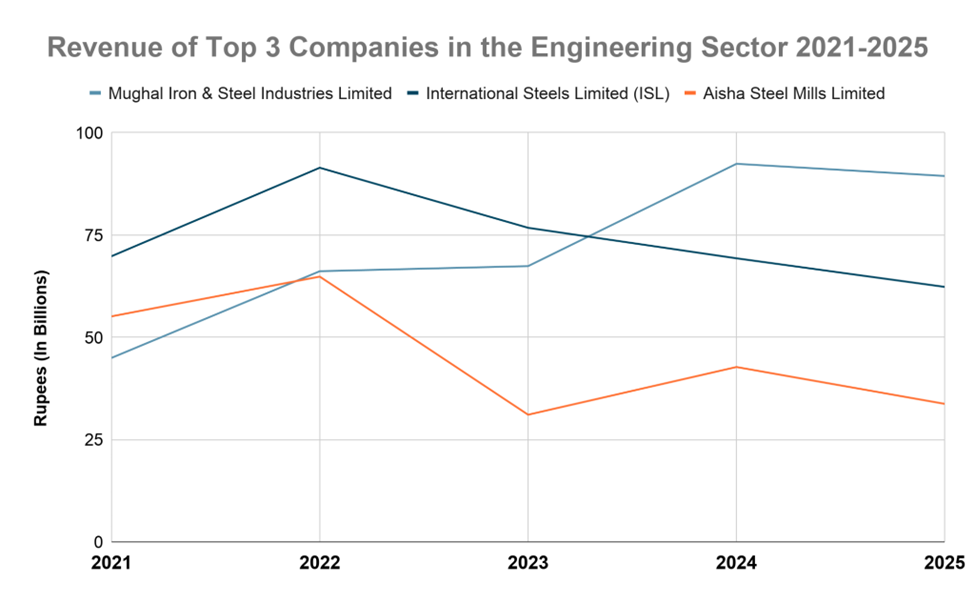

The sector reached a liquidity peak in 2022 with revenue totaling Rs. 373.42 billion. However, the projected 2025 decline to Rs. 256.41 billion represents a 31.3% contraction. This sharp reduction in top-line scale is not merely a decrease in sales volume; it represents an industry-wide struggle to maintain fixed-cost coverage. For top 3 major players, the 5-year revenue trajectory reveals a harrowing loss of momentum (See Revenue 1):

| Name of Company | 2021 | 2022 | 2023 | 2024 | 2025 |

| Mughal Iron & Steel Industries Limited | Rs. 44.97 billion | Rs. 66.15 billion | Rs. 67.39 billion | Rs. 92.38 billion

| Rs. 89.41 billion |

| International Steels Limited (ISL) | Rs. 69.80 billion | Rs. 91.42 billion | Rs. 76.75 billion

| Rs. 69.30 billion

| Rs. 62.31 billion

|

| Aisha Steel Mills Limited | Rs. 55.12 billion | Rs. 64.83 billion | Rs. 31.10 billion

| Rs. 42.75 billion

| Rs. 33.75 billion

|

This erosion of top-line revenue has catalyzed a total collapse in the sector's ability to generate bottom-line value.

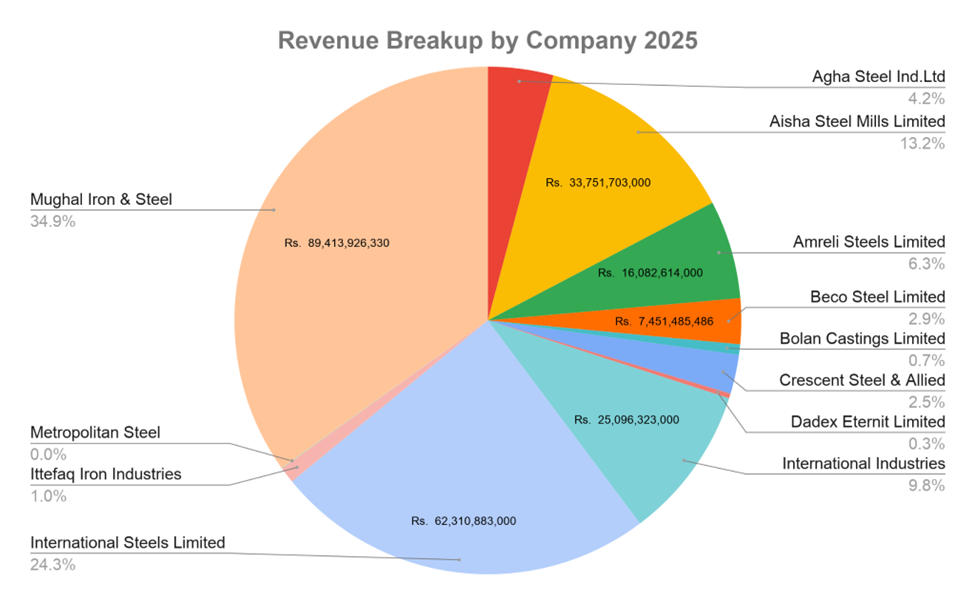

(See chart Revenue 3 for a detailed view of the main contributors to total sector revenue.)

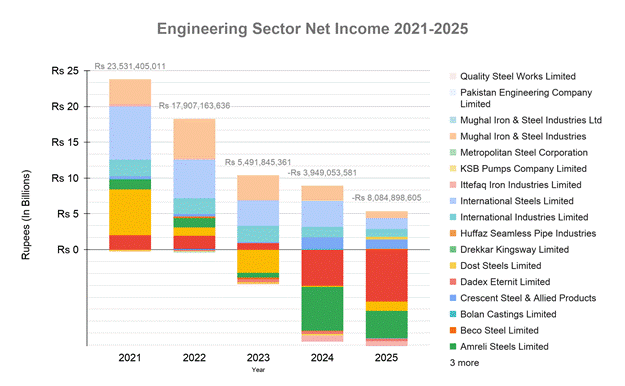

Net Income Analysis

Net Income provides the ultimate diagnostic of industrial health. The Pakistani steel sector has shifted from significant aggregate profitability to deep structural losses, a transition that calls into question the long-term viability of several Tier-1 manufacturers.

(See chart Net Income 1)

The contrast is stark: from an aggregate surplus of Rs. 23.53 billion in 2021, the sector is projected to hit a deficit of Rs. 8.08 billion by 2025. This is a massive Rs. 31.6 billion negative swing. This volatility severely compromises debt serviceability and disrupts working capital cycles, forcing firms to rely on expensive short-term borrowing to fund operations.

Specific distress cases illustrate the exponential nature of this decay:

Agha Steel Ind. Ltd: Transitioned from a profit of Rs. 2.04 billion in 2021 to a staggering projected loss of Rs. 7.21 billion in 2025. This loss is 3.5 times the size of its 2021 surplus, signaling a total breakdown in cost management.

Amreli Steels Limited: Followed a similar downward spiral, moving from a profit of Rs. 1.37 billion in 2021 to a projected loss of Rs. 3.81 billion in 2025.

These losses highlight a growing disconnect between historical operational capacity and current financial reality.

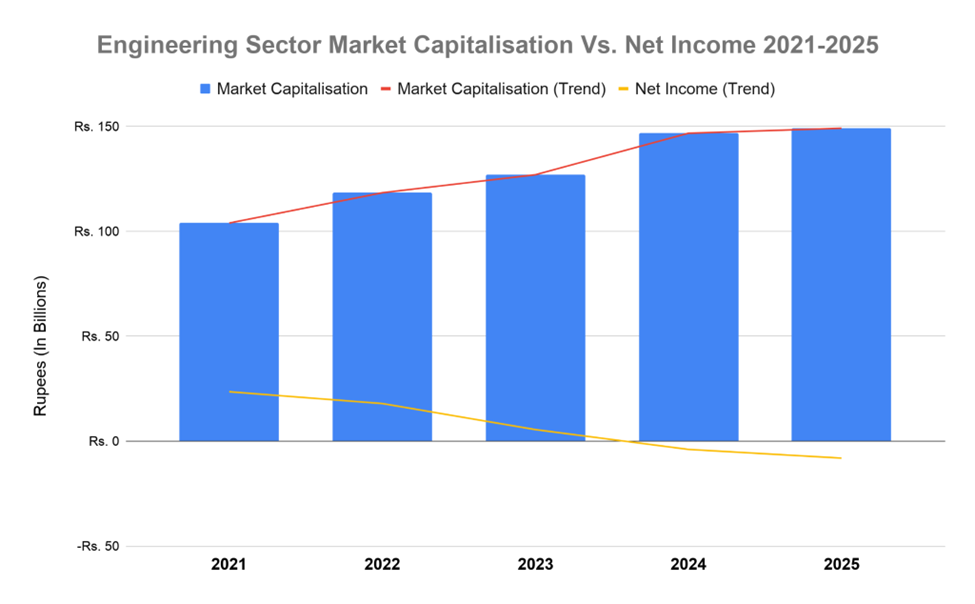

Market Capitalization vs. Operational Performance

Market capitalization should ideally track fundamental performance; however, the Pakistani steel sector presents a profound economic paradox. While net income and ROE have plummeted, the Grand Total Market Capitalization has risen from Rs. 103.92 billion (2021) to a projected Rs. 149.11 billion (2025).

This divergence likely stems from a "valuation bubble" where market pricing is driven by the inflationary revaluation of underlying physical assets—such as land and imported machinery—rather than operational cash flows. For investors, this creates a "capital trap" where equity prices are decoupled from the earnings reality of the balance sheet.

(See the table and chart: Performance Gap 1 & 2.)

The Performance Gap (2021 vs. 2025)

| Metric | 2021 Baseline | 2025 Actual |

| Grand Total Net Income | Rs. 23.53 billion | (Rs. 8.08 billion) |

| Grand Total Market Capitalization | Rs. 103.92 billion | Rs. 149.11 billion |

The widening gap as seen in the chart below suggests that market sentiment is lagging behind the severe operational decay visible in individual company performances.

Leaders and Laggards

Even in a systemic crisis, performance deltas reveal which management structures are equipped to survive prolonged economic headwinds.

Resilient Leaders

Mughal Iron & Steel Industries Limited remains the industry's outlier. Despite sector-wide contraction, it projects a net income of Rs. 965.5 million in 2025. While its ROE has compressed from 0.259 (2022) to 0.033 (2025), it remains one of the few players maintaining a positive return on its equity base. Its diversified product mix and superior cost-containment strategies provide a buffer that its peers lack.

Distressed Laggards

Agha Steel and Aisha Steel are currently the primary drivers of sector distress. Agha Steel’s ROE has collapsed to -0.344 in 2025, reflecting a complete erosion of shareholder value. Similarly, Aisha Steel Mills has been in a net loss position for three of the five years analyzed, with a 2025 projected ROE of -0.065.

Data Caveat: Notably, Dost Steels Limited shows a projected return to profit of Rs. 302 million in 2025 despite reporting zero revenue. As an analyst, this must be flagged as a non-operational anomaly, likely a result of asset divestment or financial restructuring, rather than an indicator of industrial recovery.

Industry Health

The 2021–2025 trajectory of the Pakistan steel sector indicates an industry in Critical Condition. The shift from high profitability to aggregate losses, combined with the collapse of measurable aggregate ROE, suggests that the sector's total equity is being wiped out by systemic inefficiencies and high financial leverage.

Primary Financial Threats (2025 Outlook)

Systemic Solvency Risk: The Rs. 31.6 billion swing from profit to loss has exhausted cash reserves, leaving the sector vulnerable to credit defaults.

Asset-Earnings Mismatch: A 31.3% revenue contraction since 2022 proves that the current industrial scale is unsustainable given the current demand environment.

Equity Valuation Overhang: The rising market capitalization against deepening losses creates a "valuation bubble" that is susceptible to a violent correction once the market accounts for the lack of operational cash flow.

Without immediate structural intervention, including interest rate rationalization and a major stimulus for infrastructure demand, the 2025 trajectory points toward a forced consolidation of the industry as distressed laggards face impending insolvency.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.