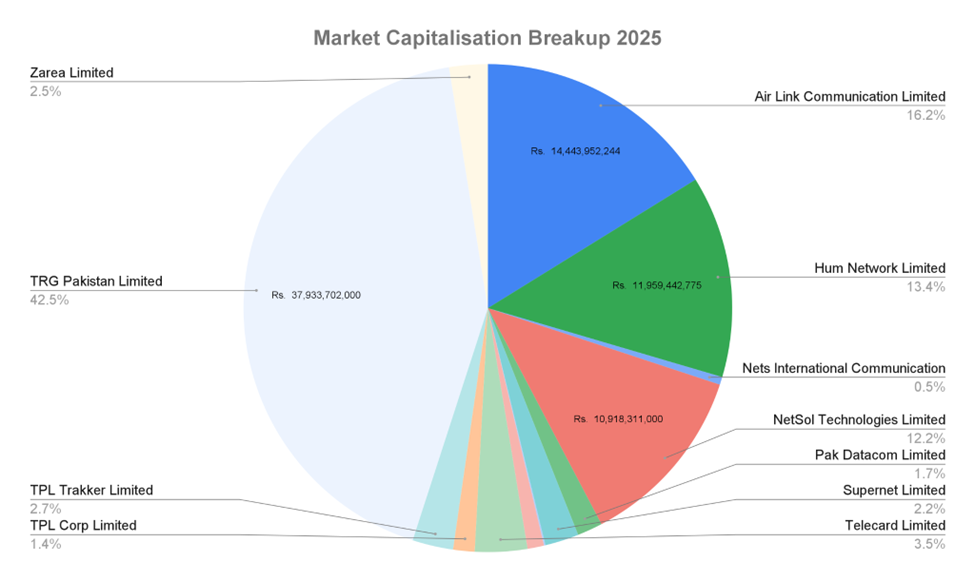

This sectoral review covers 21 listed companies operating across telecommunications, software development, IT services, digital media, and communications infrastructure. Within this group, a handful of large players continue to dominate valuation and revenue metrics, while a second tier of specialized technology firms is gradually gaining market relevance through export-oriented services and niche digital platforms. The top 5 by Market Cap. are Pakistan Telecommunications Ltd, TRG Pakistan Ltd, Air Link Communications Ltd, Hum Network Ltd and NetSol Technologies Ltd. Their sizes are seen in chart 1. {All companies are included except for PTCL, as they have not yet published their annual report for 2025.}

Between 2021 and 2025, Pakistan’s Technology and Communications sector has undergone a period of structural transition, reflecting both the country’s digital expansion and the broader pressures of macroeconomic volatility. Currency depreciation, rising operating costs, and shifting capital flows have significantly influenced investor sentiment and corporate performance across the sector. As a result, evaluating market capitalization, revenue growth, and profitability metrics has become critical for distinguishing companies with sustainable operational models from those experiencing temporary or speculative valuation cycles.

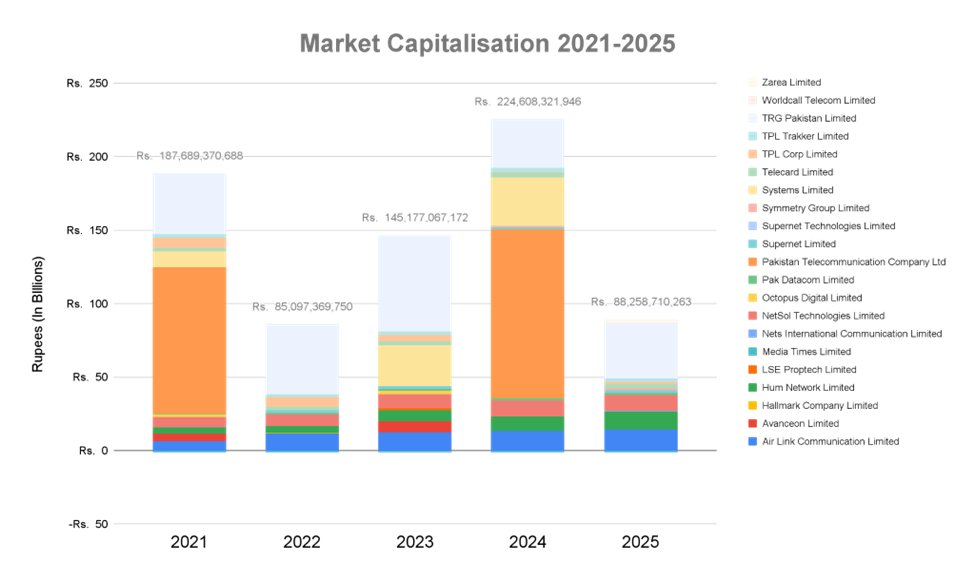

Market Capitalization Trends

Market capitalization across the sector remains heavily concentrated in a small group of dominant companies. Pakistan Telecommunication Company Limited (PTCL) continues to represent the largest valuation anchor in the sector, reaching a peak market capitalization of Rs. 115.11 billion in 2024. Meanwhile, TRG Pakistan Limited exhibited the most pronounced valuation volatility, rising to Rs. 65.50 billion in 2023 before experiencing a sharp contraction in the following year.

Among the software exporters, Systems Limited has emerged as a major growth story, reaching a peak valuation of Rs. 32.88 billion in 2024, reflecting investor confidence in Pakistan’s expanding technology export sector. Similarly, Air Link Communication Limited demonstrated steady market capitalization growth throughout the period, reaching Rs. 14.44 billion in 2025.

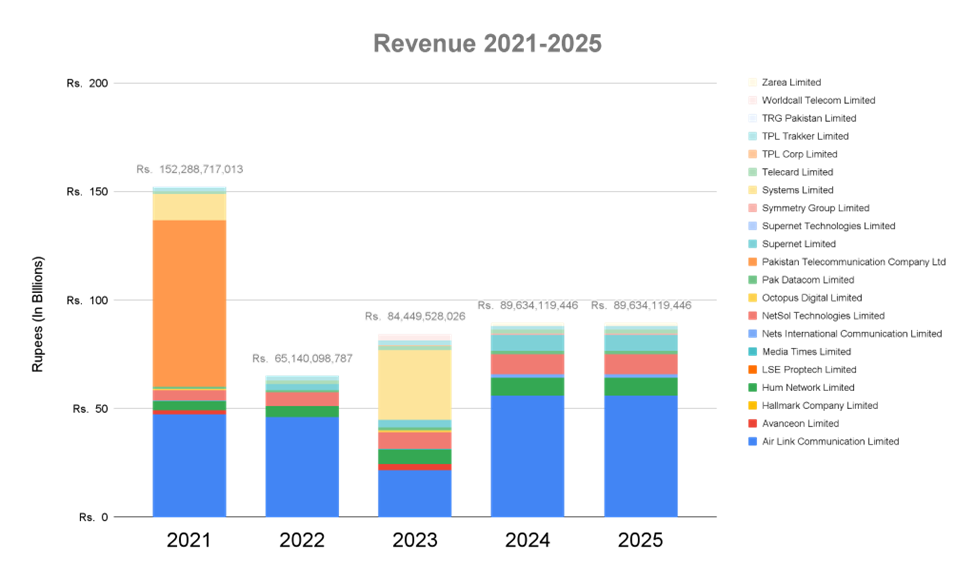

Revenue Growth and Market Expansion

Revenue performance across the sector reflects a clear divergence between hardware distribution businesses and software-driven technology exporters. While telecommunications and device distribution firms operate within capital-intensive models, software exporters have benefited from global demand for digital services and Pakistan’s growing reputation as an IT outsourcing destination.

Air Link Communication offers a notable example of volatility followed by recovery. After revenue declined to Rs. 21.50 billion in 2023, the company reported a sharp rebound to Rs. 56.14 billion in 2024, though identical revenue reporting in 2024 and 2025 suggests potential reporting rigidity or stabilization in sales activity.

In contrast, Systems Limited recorded one of the most aggressive growth trajectories within the sector. Revenue expanded from Rs. 11.90 billion in 2021 to Rs. 32.04 billion by 2023, reflecting rapid expansion in international software services and technology exports.

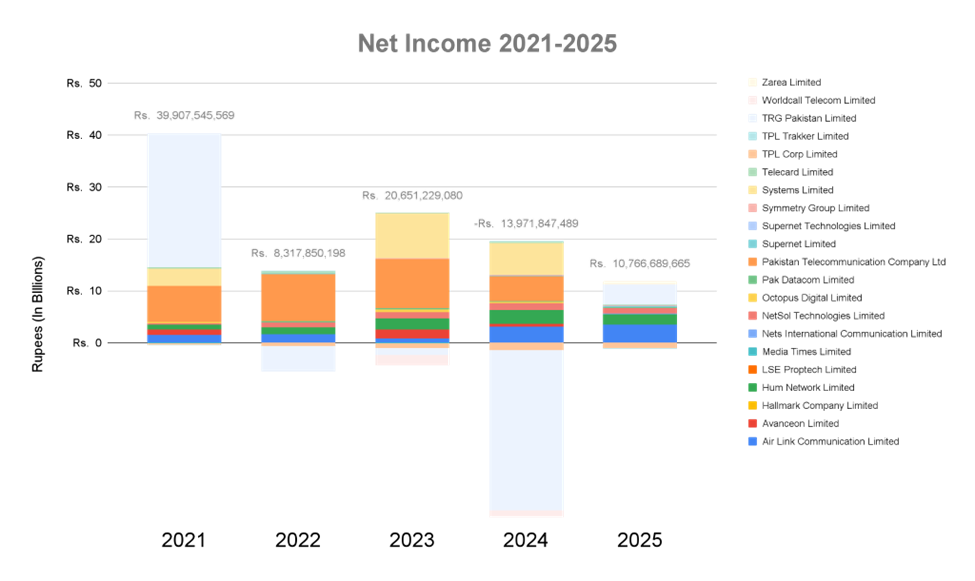

Profitability and Net Income Performance

While revenue growth provides insight into market expansion, long-term sector stability depends on the ability of firms to convert top-line growth into sustainable profitability. Over the review period, profitability outcomes varied significantly across companies.

Systems Limited maintained strong earnings momentum, recording peak net income of Rs. 8.56 billion in 2023. Meanwhile, Hum Network Limited demonstrated consistent profitability throughout most of the period, although margins declined toward the end of the cycle.

In contrast, TRG Pakistan experienced extreme earnings volatility, including a net loss of Rs. 30.85 billion in 2024, highlighting the company’s exposure to valuation-driven earnings fluctuations.

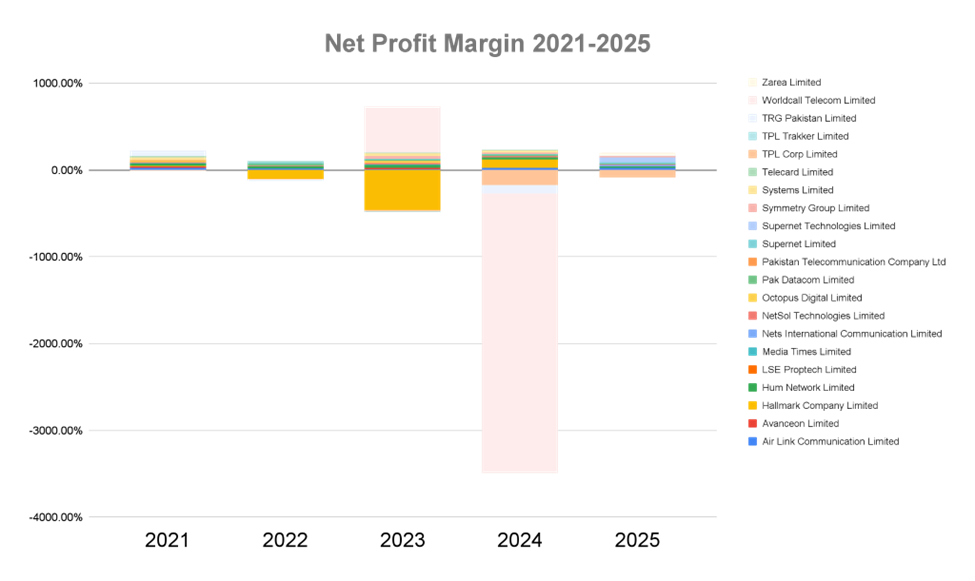

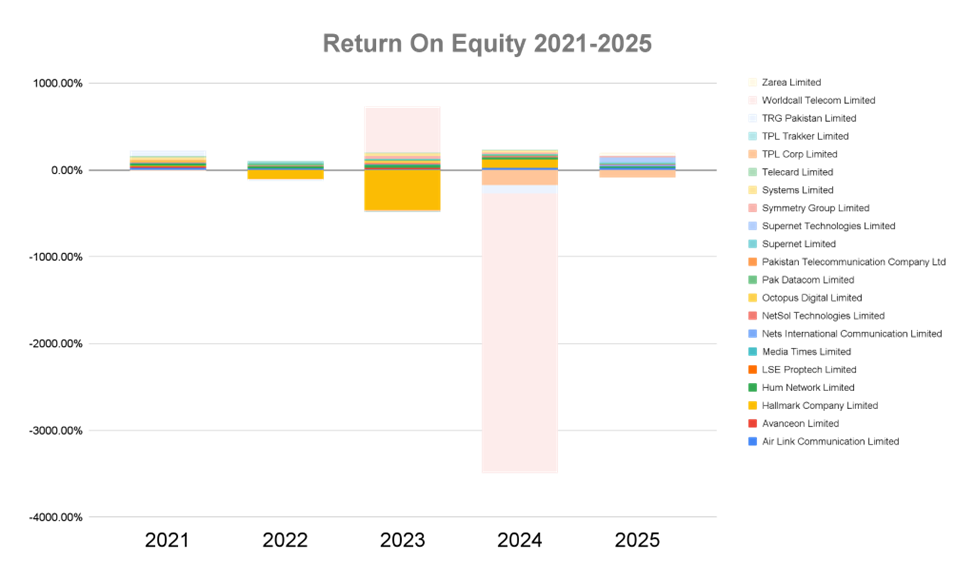

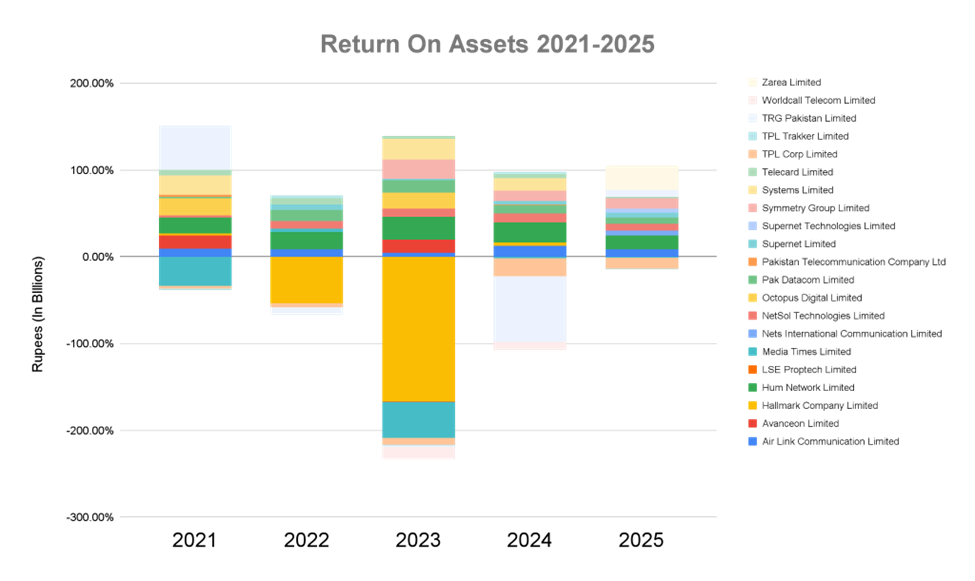

Margin Efficiency and Capital Returns

Profitability metrics further illustrate the varying operational efficiency across the sector. Companies such as Systems Limited and Hum Network maintained relatively strong net profit margins, though margin compression has begun to emerge as operating costs rise.

Return metrics also provide important insights into capital efficiency. Firms able to maintain stronger Return on Equity (ROE) and Return on Assets (ROA) have generally demonstrated stronger governance, cost discipline, and operational scalability.

Sector Outlook

Taken together, the data suggests that Pakistan’s Technology and Communications sector is entering a phase of strategic differentiation rather than uniform expansion. Large telecommunications operators continue to dominate valuation metrics (with a historical growth rate of 8%), while software exporters and specialized technology firms are increasingly driving innovation and profitability (with a year over year growth of 10% in Net Profit Margins).

As digital services demand expands globally, firms capable of maintaining revenue growth while preserving margins are likely to attract institutional capital. At the same time, financially distressed or highly volatile entities may face increasing pressure from investors and regulators as the sector moves toward greater consolidation and operational transparency. This is due as most of the innovators in the space have little regard for documentation of processes, a key part of developing transparent organisational policies.

Disclaimer: This content is published solely for awareness, educational, public information, and journalistic purposes. All data is sourced from Pakistan Stock Exchange (dps.psx.com.pk) and relavant companies website.